Full version overhaul: OIPD now fits an arbitrage-free volatility surface, and uses this to compute implied probability distributions

Now we provide 2 capabilities:

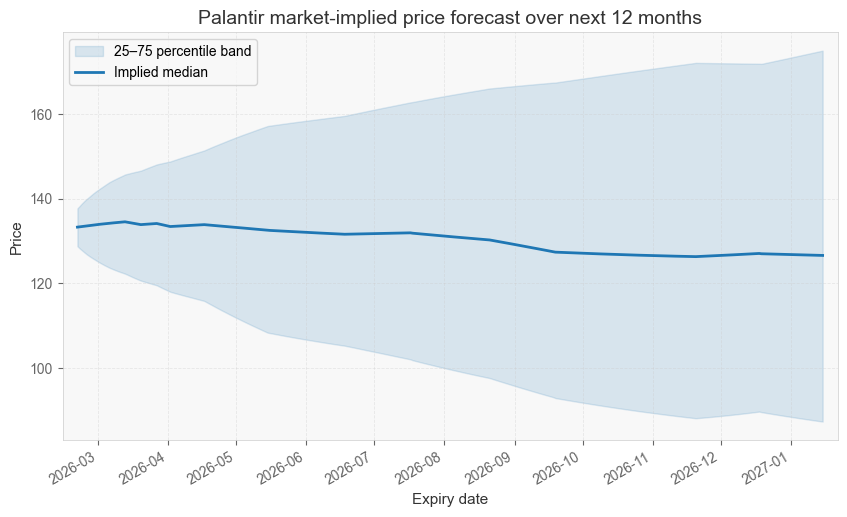

- It computes the market's expectations about the probable future prices of an asset, based on information contained in options data.

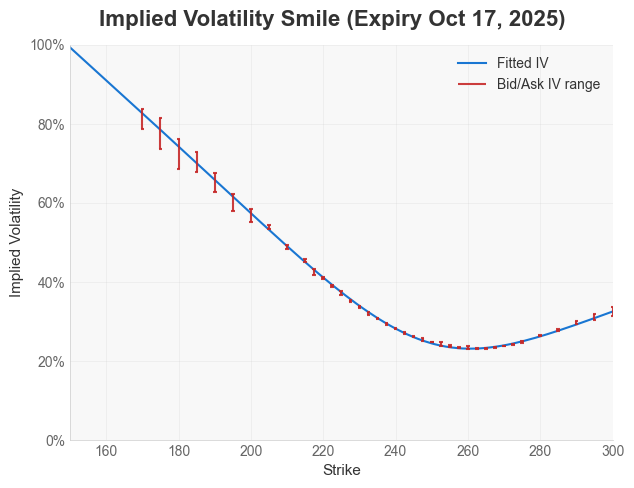

- For options traders, it also offers a simple-to-use but rigorous pipeline to fit an arbitrage-free volatility smile/surface (using SVI under the hood), which can be used to price options.

The API has been overhauled.

Sorry, this is a breaking change. The previous API was strictly designed for inferring probabilities, as we didn't expect to offer volatility fitting. So we redesigned the API, it should be more intuitive to use, and should be future-proof and stable now.

Documentation is still WIP

We have some example Jupyter notebooks, but the full documentation and technical detail & theory is still being worked on. I'm looking to complete that in the coming week.